What does the phrase ‘green finance’ mean to you, if anything?

A colleague made this for the finance team recently (I think he takes orders, if you’re interested), so perhaps this is his interpretation of ‘green finance’? There are three of us in the team. I daren’t ask which might be me.

But more commonly green finance refers to financial products and services that are being managed carefully to minimise negative impacts on the environment.

Just as you might think about the ingredients and packaging when choosing a shampoo, you can look at the underlying investments of banks, insurance companies and investment funds when choosing where you put your money.

Note of warning – as with everything ‘green’, there is always the potential for greenwashing. Since I started researching for this blog, I’ve been getting more and more adverts popping up: ‘a nicer kind of ISA – helps cut carbon emissions from schools’; ‘solar on big roofs just makes sense, buy shares and join our cooperative to help make it happen’’; etc. These products may be legitimate, but it’s worth flagging up that you do need to use your research skills if you want to make greener financial choices, to avoid being mis-sold or even scammed.

So, what can we look at to make our finances more “green”?

Bank accounts are a good starting point, as we all need to have them. Many of us sign up to a current account with freebies, such as a 4-year railcard for students, or a cashback deal for switching. But there are a huge number of current accounts these days, and the ones with the biggest budgets to bribe us may not have the best environmental credentials. Take the time to research banks and what they do with your money.

There are many places to look for this information, but the following suggestions have all come from a campaign called Make My Money Matter. Despite the campaign closing in 2025 (because the organisers feel they’ve achieved their aims) the site is still worth looking at because it has lots of interesting resources. The campaign wanted ‘to raise awareness and drive action around the power of our pensions and banks to tackle – rather than fuel – the climate crisis.’

The three main areas they addressed were banks, advocacy and pensions.

I still remember being irritated hearing from my bank manager for the first time. (Does anyone ever hear from their bank manager anymore?). I’d got my first proper job and my student account had morphed into a graduate account. I got my first ever monthly salary from a full-time job – yay! And suddenly there was the bank manager on the phone, talking about pensions and investments, and other things I’d never heard of. My first paycheck, and he wanted to take it away!!!! I ignored him. But, after a while, I realised I probably did need to think about it.

By the way, if you haven’t thought much about saving for the future, food storage is a useful analogy. Try to fill your fridge first, and then start to stack the larder.

When you get a regular job, your employer will enrol you on to a pension, so you will be adding items to your freezer. Please, please, please, psych yourself up to read the blurb that comes with it, especially the way that YOUR pension contributions are being invested. It’s YOUR money, that’s being invested to build up for YOUR later life.

Some pension schemes only have a default setting, but most allow you to make choices of where the money is invested. The choices you make will affect the amount of ££££s you end up with, but also make a huge difference to the environment. Some investments simply avoid environmentally-damaging companies, such as oil companies. Others actively invest in green technologies such wind turbine manufacturers. And there are no crystal balls to help you find this information, despite how confident any advisers may sound. But doing nothing and just accepting the default option is also a choice that you are making. Green finances rely on some researching and input from you about what you want your money invested in.

All of this applies if you also decide to invest in stocks ISAs/shares/myriad other products that come with that warning you often hear garbled at the end of adverts – ‘the value of your investment can go down as well as up’.

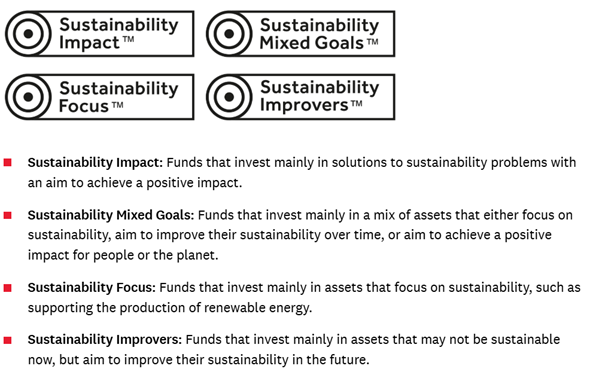

There are so many choices, it is daunting. The government body that tries to make sure financial services behave themselves is the FCA (Financial Conduct Authority). They’re working on a labelling regime for investments that have environmental goals, so we should hopefully start to see these labels on investment products, just as we see the traffic light labels on food products, to help us have confidence in our choices. This will help us more easily identify options that help us use our money to support sustainable initiatives, so look our for these in the future.

Remember that while big companies have a lot of power over environmental solutions, actions and decisions by individuals can have a big impact too. Changing daily habitats, making eco-friendly swaps and using our finances in a more sustainability-focused way will have a huge impact, especially if you advocate for these changes to friends and family.

Consider if you want to make any changes to where you’re keeping your money, and research companies that match your values. Green finance is important!

*****

P.S. If you’d like to improve your financial capability generally……

I recommend looking the Martin Lewis MSE website before almost every financial decision. There are different sections for every type of financial transaction you’re ever going to make, explaining things, comparing best buys and even offering some discounts.

He’s also helped to develop the free ‘MSE’s Academy of Money’ course provided by The Open University if you’re really keen!

© 2026 Operation Wallacea Ltd. Website by Yello Media.

Social Media Links